NHS Pensions and Divorce: What Every Doctor Needs to Know

For many doctors, their NHS pension is one of the most valuable assets they will ever own. Yet it is also one of the least understood.

Unlike a personal pension or investment fund, an NHS pension is a defined benefit scheme with its own rules, different scheme sections and unique valuation issues. Decisions made during divorce can affect your retirement income for decades.

Perhaps most importantly, the figure shown on your annual NHS pension statement may not tell you what your pension is really worth in the context of a divorce. Understanding how an NHS pension should be treated as part of a financial settlement is often far more complex than many doctors initially realise.

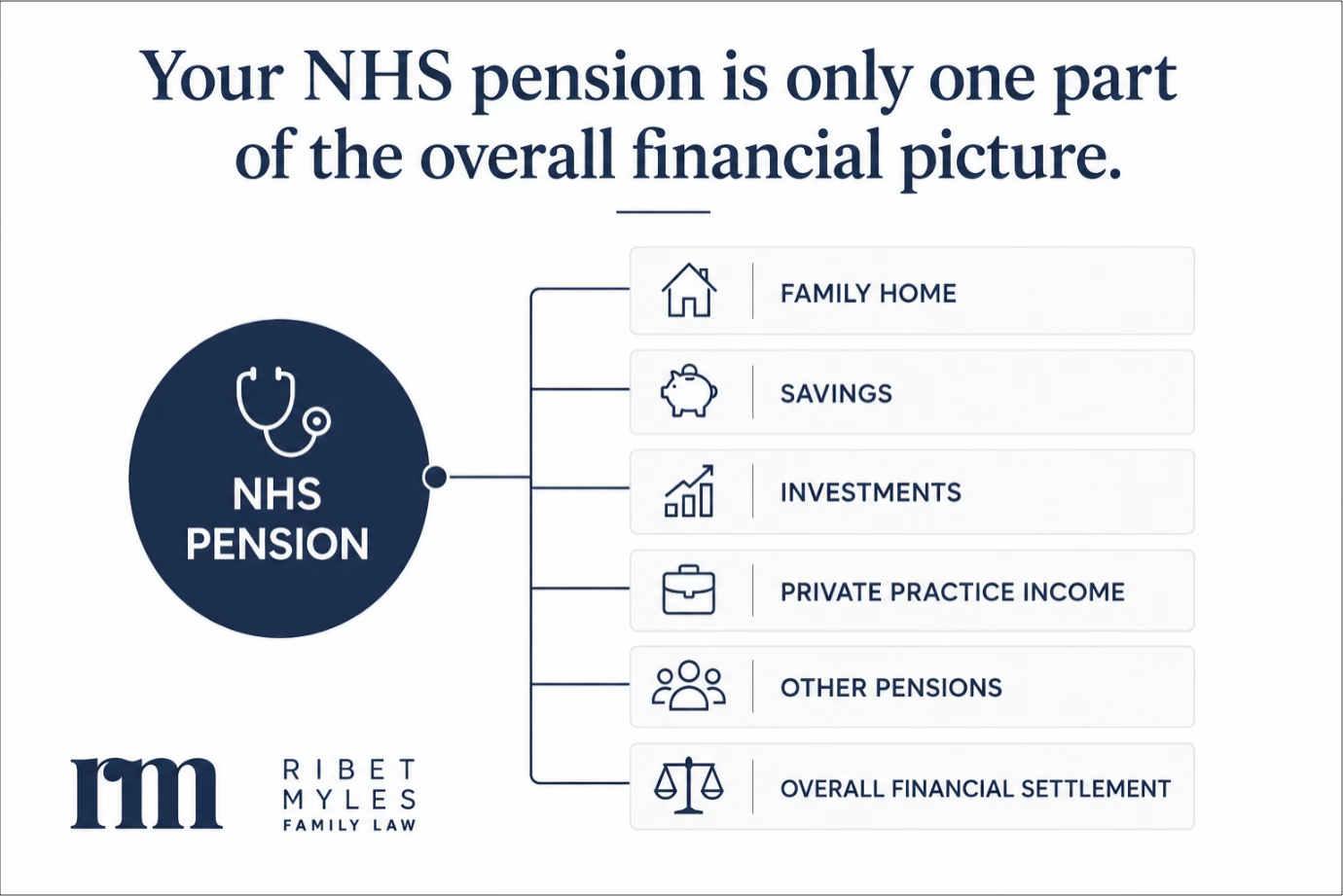

That doesn't mean every doctor needs an actuarial report or that every NHS pension must be shared. It does mean that an NHS pension should never be viewed in isolation. Like the family home, savings, investments and any private practice interests, it forms part of the overall financial picture that needs to be considered during a divorce.

At Ribet Myles, we regularly advise consultants, surgeons, GPs and other medical professionals on complex financial settlements. Where specialist pension expertise is required, we work alongside experienced pensions-on-divorce experts to ensure every aspect of the settlement is properly considered.

Learn more about divorce for doctors

Why NHS pensions deserve specialist attention

No two NHS pension cases are identical.

Two doctors with apparently similar pension statements can have very different retirement benefits depending on their NHS service, pension scheme membership, career history and future retirement plans. That's one reason why it is unwise to make assumptions based solely on headline pension values.

Most family solicitors deal with pensions. Comparatively few regularly advise doctors on the unique issues surrounding NHS pension benefits, GP partnerships, private practice income and complex medical careers.

NHS pensions and divorce: the key points

Before looking at the detail, there are several important points every doctor should understand.

Your NHS pension is likely to be taken into account as part of your financial settlement.

Your spouse is not automatically entitled to half of your NHS pension.

The value shown on your pension statement may not tell the whole story.

NHS pensions are significantly more complex than many private pensions.

Decisions about your pension should never be made in isolation from the rest of your financial settlement.

What happens to an NHS pension when you divorce?

When a marriage ends, the court looks at the parties' overall financial circumstances. An NHS pension is one of the assets that may be considered alongside:

the family home;

savings and investments;

other pensions;

business interests;

private practice income;

future earning capacity; and

each person's financial needs in retirement.

There is no automatic rule that says your spouse will receive half of your NHS pension.

Instead, the court's objective is to achieve a fair outcome based on the particular circumstances of your case.

For one couple, that may involve sharing part of the pension.

For another, it may be fair for one spouse to retain the pension while the other receives a larger share of the family home or other assets.

Every case is different, and the right approach will depend on your individual circumstances.

Why are NHS pensions different?

Many people think of pensions as investment pots containing a fixed amount of money.

An NHS pension is different.

It is a defined benefit pension, meaning it provides retirement benefits calculated under the rules of the NHS Pension Scheme rather than simply reflecting the amount that has been paid into an investment account.

For doctors, this creates a number of additional issues.

Many have pension benefits built up in different sections of the NHS Pension Scheme, including the 1995, 2008 and 2015 schemes. Each operates under different rules and may have different retirement ages and benefit structures.

Doctors may also have a combination of NHS pension rights, private pensions and income from private practice, all of which need to be considered as part of the wider financial picture.

For that reason, decisions about an NHS pension should rarely be based solely on the figures shown on an annual statement.

This doesn't mean your pension cannot be valued fairly. It does mean that understanding what those benefits are worth—and how they should be treated within a financial settlement—can require considerably more analysis than many people expect.

What is a Cash Equivalent Transfer Value (CETV)?

During divorce proceedings, you will usually need to obtain a formal valuation of your pension.

This is known as the Cash Equivalent Transfer Value, or CETV.

Many doctors understandably assume that this figure represents what their NHS pension is worth.

In reality, it is a valuation prepared for pension purposes and, whilst it is an important starting point, it does not necessarily tell the whole story.

For example, it does not explain:

how much retirement income the pension is likely to provide;

how different retirement ages may affect the benefits;

whether two pensions with similar CETVs will produce similar incomes;

whether exchanging pension rights for other assets would be fair.

One of the most common misunderstandings is assuming that the CETV of a pension is automatically equivalent to the same amount of equity in a house.

In reality, it is rarely that straightforward. Understanding what the CETV means — and just as importantly, what it does not mean — is an important part of assessing how your NHS pension should be treated on divorce.

Pension sharing or pension offsetting?

Many doctors are surprised to discover that there is more than one way an NHS pension can be dealt with on divorce.

The two approaches most commonly considered are:

Pension sharing

A pension-sharing order transfers a percentage of pension rights to the other spouse, who then has pension rights in their own name.

Pension offsetting

Instead of sharing the pension, one spouse keeps more of the pension while the other receives a greater share of other assets, such as the family home or investments.

Which approach is best depends entirely on the circumstances.

A doctor approaching retirement may have very different priorities from a younger GP partner still building their career.

Similarly, retaining a valuable NHS pension may appear attractive, but only if the overall financial settlement remains fair.

The right answer depends on the wider financial picture rather than the pension in isolation.

Why doctors often need specialist advice on divorce

Most divorces involving pensions can be dealt with using standard pension information.

However, NHS pensions can present additional complexities that require careful consideration.

These may include:

membership of more than one NHS pension scheme;

GP practitioner and hospital service;

significant private practice income;

substantial pension values;

approaching retirement;

pensions already in payment;

questions about benefits built up before the marriage;

proposals to offset the pension against the family home.

In some cases, a specialist pensions-on-divorce expert (often called a PODE) may be asked to prepare an independent report.

That expert's role is not to replace your solicitor but to provide technical pension analysis where it is needed.

Your solicitor does not need to be an actuary. They do, however, need to recognise when specialist pension evidence is required, ask the right questions and use that advice to negotiate the best possible financial settlement.

What is the McCloud remedy?

If you have been a member of the NHS Pension Scheme for a number of years, you may have heard references to the McCloud remedy.

This arose following changes made to public sector pension schemes in 2015.

Those reforms moved many members into the newer 2015 NHS Pension Scheme. However, the courts later decided that some of the transitional arrangements unfairly disadvantaged certain members because of their age.

As a result, the Government introduced what is known as the McCloud remedy to correct those issues.

For some NHS staff, this means pension benefits built up between 2015 and 2022 may need to be reconsidered under revised rules.

You do not need to understand the detailed legal and actuarial mechanics of the McCloud remedy.

What matters is recognising that, for some doctors, it can affect pension valuations used during divorce proceedings.

If the McCloud remedy is relevant to your circumstances, your solicitor can ensure it is taken into account and obtain specialist advice where necessary.

Key Questions Before Reaching a Financial Settlement

1. Will my spouse automatically receive half of my pension?

There is no automatic 50:50 rule.

2. Have you looked beyond the CETV?

The Cash Equivalent Transfer Value (CETV) provides a formal valuation of your NHS pension, but it doesn't always answer the questions that matter most during a divorce. For example, it may not indicate how much retirement income the pension is expected to provide or whether it can be fairly compared with assets such as the family home. Looking beyond the headline figure can make a significant difference to the overall financial settlement.

3. Are you comparing your pension fairly with your other assets?

An NHS pension and property are fundamentally different assets. While it may be tempting to think that a pension worth £500,000 is equivalent to a house with £500,000 of equity, that is often an oversimplification. They provide different types of financial security, are treated differently for tax and retirement purposes, and comparing them fairly usually requires careful legal and, in some cases, specialist pension advice.

4. Are you making decisions too early?

Agreeing a settlement before understanding your pension can be an expensive mistake.

5. Are you treating your pension separately from everything else?

The pension is only one part of the overall financial settlement.

“Your NHS pension may be one of your most valuable assets—but the figure on your annual statement doesn't always tell the whole story.”

Frequently asked questions

Can my spouse take my NHS pension?

This is unlikely, although they may be entitled to a share. Your NHS pension may be taken into account during your divorce, but that does not mean your spouse will automatically receive part of it. The outcome depends on your overall financial circumstances and the terms of any financial settlement.

Can I keep my NHS pension?

Possibly. In some cases, it is appropriate for one spouse to retain their pension while the other receives more of the available capital. Whether this is suitable depends on the overall fairness of the settlement.

Is the value shown on my NHS pension statement the amount my spouse will receive?

No. The valuation shown on your statement is only one factor considered during divorce and should not automatically be treated as the amount that will be shared.

Why is it important to understand my NHS pension before negotiating?

Important decisions about pensions are often made at the beginning of financial negotiations rather than the end. Taking time to understand how your NHS pension fits into the wider financial settlement can help you make informed decisions from the outset.

The biggest risk isn't necessarily losing part of your NHS pension. It's making decisions about it before you fully understand what it's worth and how it fits into your overall financial settlement.

Do I need a pensions expert?

Not every case requires one. However, where NHS pensions are particularly valuable or complex, or where there are questions about valuation or offsetting, specialist pension advice can be invaluable.

How Ribet Myles can help

If you're a doctor, consultant, surgeon or GP facing divorce, understanding your NHS pension should be one of your first priorities—not your last.

At Ribet Myles, we regularly advise medical professionals on complex financial settlements involving NHS pensions, private practice income, GP partnerships and other specialist issues. We understand the legal complexities surrounding NHS pensions, recognise when specialist pension evidence is required and work closely with experienced pensions-on-divorce experts where appropriate.

Our aim is simple: to help you achieve a fair financial settlement that protects your long-term financial security while reflecting your pension, your home, your other assets and your future retirement plans.

If you're concerned about how your NHS pension may be affected by divorce, call us on 020 7242 6000 to arrange a complimentary 30-minute consultation with one of our experienced family lawyers.

Early advice can help you understand your options before important decisions are made, giving you the confidence to move forward and achieve the best possible financial outcome for you and your future.

This article provides general information about divorce and NHS pensions in England and Wales. It is not legal, financial or actuarial advice. Every case is different, and you should obtain advice tailored to your individual circumstances before making decisions about your financial settlement.